There are two types of conversations in moving:

Customer: “Everything I own is priceless.”

Carrier: “Let’s put a number on that.”

Welcome to Full Value Protection (FVP) — where federal law, math, and mild anxiety all ride in the same truck.

The Law Says You Must Offer It (Even If You Make That Face)

“Yes, we have to talk about valuation.”

“No, ‘good luck’ is not a compliant option.”

Under FMCSA regulations, interstate movers must offer:

- Full Value Protection (FVP)

- Released Value (60 cents per pound per article)

Released Value is:

“If it’s heavy, you’re covered. If it’s expensive… we’ll discuss.”

FVP is:

“Let’s agree on responsibility now, so we don’t argue later.”

FVP means the carrier is responsible for repair, replacement, or settlement — within the declared value of the shipment.

And yes – customers pick this more often than carriers would prefer.

The Big Picture (Before We All Start Dividing by 1,000)

Before we even talk dollars, FVP always comes down to three moving parts:

Step 1: Declared Shipment Value → What is everything worth?

Step 2: Deductible Selection → Decide how much risk everyone keeps?

Step 3: Valuation Charge Rate → What does this protection cost? Yes, it’s math. Try not to panic.

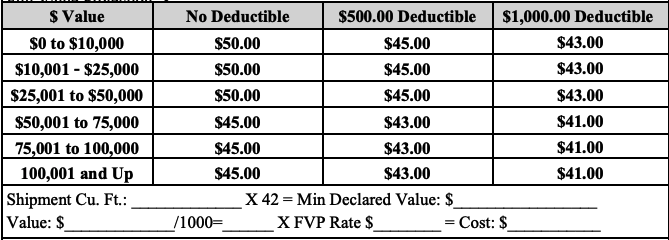

Declared Shipment Value Price Table & Deductibles

Step 1: The $6 Per Pound Rule (Not a Suggestion, Not a Guess)

“Minimums exist for a reason – mostly legal ones.”

If the customer doesn’t declare a value, federal rules default the shipment value calculation to:

$6.00 × weight (in pounds)

(with a $6,000 minimum)

So:

10,000 lbs = $60,000 declared value

This isn’t random – it’s a baseline safeguard for your liability level:

- Protects the customer from accidentally under-valuing everything

- Protects the carrier from “this whole house is worth $4,000” conversations

It’s essentially DOT saying:

“We’re not leaving this up to vibes.”

Customers can declare higher values – especially for high-value items – but they must do so before the move, not during the claim when suddenly everything is antique.

Step 2: Deductibles: Where the Risk Gets Shared (and the Tone Changes)

“Ah, yes. The part everyone suddenly understands.”

FVP isn’t just one number — it often includes deductible options:

- $0 deductible (premium price, premium expectations)

- $500 deductible

- $1,000 deductible

This is where the conversation gets real:

Customer: “I want full protection.”

Carrier: “Perfect. How much risk would you like to keep?”

Higher deductible = lower upfront cost

Lower deductible = fewer uncomfortable conversations later

Step 3: The Math (a.k.a. Where the Tariff Gets Involved)

“Relax. It’s just multiplication wearing a uniform.”

Now we combine everything:

FVP Charge = (Declared Value ÷ 1,000) × Rate per $1,000

Example:

Declared shipment value: $60,000

Rate of FVP: $45 per $1,000 of shipment value

FVP cost to customer: (60,000 ÷ 1,000) × $45 = $2,700

Adjust the deductible → adjust the rate → adjust the price

That’s exactly what your tariff tables are doing:

Translating risk into dollars… with very official formatting.

Okay, But When Something Breaks… Then What?

“This is the part nobody reads until they really, really need to.”

Now that we’ve:

- Set the shipment value

- Chosen the deductible

- Charged the customer

We’ve already defined how compensation works.

Under FVP, the carrier must:

- Repair

- Replace with like kind and quality

- Or settle for the cost

But always within:

- The declared value ceiling

- Minus the deductible

Compensation Example (a.k.a. Let’s See If We Did This Right)

Customer selected:

- Declared value: $60,000

- Deductible: $500

Damage:

Dining table repair = $1,200

Outcome:

- Customer pays first $500

- Carrier pays $700

Everyone:

“This is not ideal… but at least it makes sense in a structured, federally compliant way.”

Why Carriers Should Actually Care (Yes, Even Financially)

“Let’s address the elephant in the truck.”

Carriers think they prefer 60 cents per pound because:

- It’s cheaper

- It’s predictable

- It avoids big payouts

But here’s the reality:

FVP is structured risk the customer pays for upfront.

Which means:

- Claims are partially offset by deductibles

- Coverage is funded through valuation charges

- Expectations are clearly documented

So instead of:

Customer: “Surprise, this is expensive.”

You get:

Carrier: “We already agreed how this works.”

And when things go completely off the rails?

That’s when you call your cargo insurance and say:

“Hey… remember me?”

Final Thought: FVP Isn’t Expensive – Confusion Is

FVP doesn’t create risk. FVP is paid risk.

FVP doesn’t eliminate problems – it just makes them harder to argue about later… and already priced into the conversation. FVP just makes sure everyone agreed on the risk in advance.

Which, in moving, is about as close to peace of mind as it gets. 🚛